Update June 2025: This offer now appears to be severely limited very soon to occasional gift cards.

Update April 2025: I’ve continued to receive my $5 in SBUX credit every week with no issues, up to over $50 so far. Honestly, getting $5 worth of caffeine every week feels better than it should, no wonder Starbucks is effectively running its own currency. You do need to remember to log into the app every week (Fridays for me, not sure if same day for everyone). Now you can either sign up for Starbucks or Dunkin credit (thanks to DoC).

You can still get an additional one-time $5 cash bonus if you open through Aven.com/advisor and use my invite code JP25DJVG7K during the app sign-up. You’ll need to link a bank account via Plaid to get the $5 transferred to you.

Some caveats: Don’t accidentally sign-up for their credit card, it is not required to get this $5 weekly credit. They have also added new fine print that the offer is limited to residents of AL, AK, AZ, AR, CA, CO, FL, GA, ID, IL, IN, IA, KS, KY, LA, ME, MD, MI, MN, MS, NE, NH, NJ, NM, NC, ND, OH, OK, OR, PA, SD, TN, UT, VA, WI, WY. This was not the case originally.

Original post from 2/3/2025:

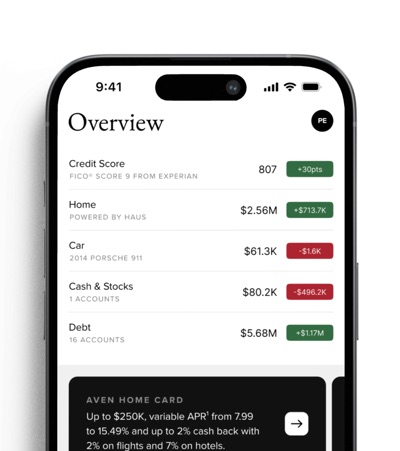

Aven Advisor is a new app that promises to help to track your financial situation. Kind of like the old Mint app, you have to give them your personal info and link up bank accounts/credit cards, and then they offer a unique mix of things:

- Free weekly credit score (VantageScore 4.0 for me, even though some screenshots show FICO).

- Find your hidden subscriptions by mining your transactions.

- Track your home value, neighborhood home prices, and show you nearby house listings.

- Get a free lien report on your property.

- Track your bank balances, brokerage balances, and credit card debt.

- Track the value of your car.

- Shows you nearby Facebook Marketplace listing for cars and other random things.

So why give them your data? Well, if you are a homeowner with a good credit (700+), they will give you $5 in Starbucks credit once every week. You have to manually open the app and tap the link on every Monday (so they know you’re actively using it), but I’ve successfully gotten my credit. Loads right onto my Starbucks app, see screenshot below.

Join at Aven.com/advisor (remember, only homeowners get the Starbucks offer). You can also get an additional one-time $5 cash bonus with my referral code JP25DJVG7K. Thanks if you use it. You’ll have to link a bank account via Plaid to transfer the $5 into your account.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)