The card_name is their no-annual-fee travel rewards card with 1.25x miles on all purchases. There are bigger rewards and bonuses from the premium Capital One Venture and ultra-premium Capital One Venture X cards, but this card still offers a 20,000 mile bonus with a lower spending requirement and no annual fee. 20,000 miles can be redeemed for $200 in travel, offsetting any travel purchase made with the card (any airline, any hotel, AirBNB stays, Uber rides, no blackout dates). This is also the rare card that allows your points to transfer to airline miles without an annual fee. Here are the highlights:

- For a limited time, enjoy a $100 credit to use towards flights, stays and rental cars booked through Capital One Travel during your first cardholder year. Plus, earn 20,000 bonus miles once you spend $500 on purchases within the first 3 months from account opening.

- Earn unlimited 1.25X miles on every purchase.

- Enjoy 0% intro APR on purchases and balance transfers for 15 months; reg_apr,reg_apr_type APR after that; balance transfer fee applies

- Miles won’t expire for the life of the account and there’s no limit to how many you can earn

- 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel.

- Use your miles to get reimbursed for any travel purchase – or redeem by booking a trip through Capital One Travel

- Transfer your miles to your choice of 15+ travel loyalty programs.

- No foreign transaction fees.

- $0 annual fee.

Travel statement credit redemption details. Capital One “miles” can be redeemed directly for a cash statement credit on a 1 mile = $0.01 basis when offsetting any travel purchase made on the card within the past 90 days. In other words, 40,000 miles = $400 toward travel. That means you can fly on any airline or stay at any hotel, pay with this card, and then “erase” that purchase using your miles balance later. This even includes AirBnB vacation rentals, car rentals, and Uber rides.

This means that earning 1.25 miles on on every $1 in purchases essentially makes this a flat 1.25% back card when applied towards travel. You also have the option of booking travel through their travel portal, similar to Chase Ultimate Rewards, but you are not required to do so. You have the flexibility of booking through them or making the purchase directly through the airline, hotel, car rental counter, etc.

Miles transfer options. Capital One now allows you to transfer your “miles” into select airline miles programs as well. Here are the airline transfer partners:

- Aeromexico

- Air France/KLM

- Air Canada Aeroplan

- Cathay Pacific Asia Miles

- Avianca Lifemiles

- British Airways Avios

- Emirates Skywards

- Etihad

- EVA

- Finnair

- Qantas

- Singapore Airlines Krisflyer

- TAP Air Portugal

- Turkish Airlines

- Virgin Red

Hotel partners

- Accor Live Limitless

- Choice Hotels

If you are willing to do some research on how to best leverage these international airline miles programs, this can be a very valuable option. (My personal favorite is Air Canada Aeroplan points.) Otherwise, it’s nice to know you can always get a certain level of value by redeeming against any travel purchase.

Comparison with other travel cards. This VentureOne Rewards credit card earns 1.25x miles on all purchases with no annual fee, and has the capability on its own to transfer to airline miles. The Chase Freedom Unlimited card earns 1.5 Ultimate Rewards (UR) points per dollar spent with no annual fee, but it does not allow you to transfer the points to airline mile partners on its own. You must first transfer the UR points to another Chase Sapphire card that has an annual fee. You may also consider this VentureOne card as a downgrade option for other Venture cards, given its no annual fee and ability to keep your miles redeemable and transferrable (but with lower earning rates and fewer features).

Capital One’s “premium” card is the Venture Rewards credit card, which is more directly competitive with the Chase Sapphire Preferred.

Capital One’s “ultra-premium” card is the Venture X Rewards credit card, which has more perks including Priority Pass airport lounge access and a $300 annual travel credit through Capital One Travel, but also a higher $395 annual fee. The Venture X competes more directly with the Chase Sapphire Reserve.

Bottom line. The card_name earns 1.25x miles on all purchases, which you can either redeem against any travel purchase or transfer to one of their airline/hotel partners. Right now, there is a 20,000 bonus miles offer for new sign-ups, worth $200 towards travel.

Also see: Top 10 Best Credit Card Bonus Offers.

Here’s my monthly roundup of the best interest rates on cash as of February 2023, roughly sorted from shortest to longest maturities. We all need some safe assets for cash reserves or portfolio stability, and there are often lesser-known opportunities available to individual investors. Check out my

Here’s my monthly roundup of the best interest rates on cash as of February 2023, roughly sorted from shortest to longest maturities. We all need some safe assets for cash reserves or portfolio stability, and there are often lesser-known opportunities available to individual investors. Check out my

Capital One 360 has a new special

Capital One 360 has a new special  Primis Bank is relatively unknown, but is sure to gather some new deposits with their

Primis Bank is relatively unknown, but is sure to gather some new deposits with their

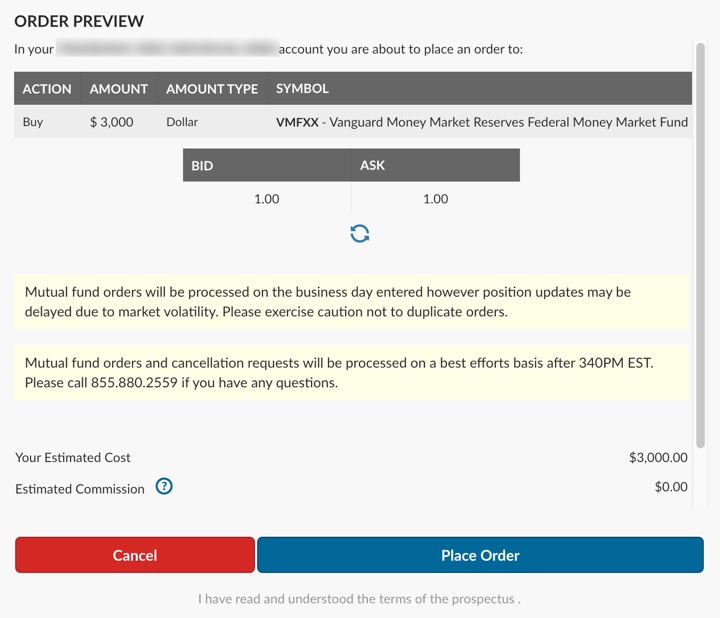

While updating my posts on

While updating my posts on

Investing app Public just announced a

Investing app Public just announced a  The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)