![]()

New promo. Plastiq has a new promotion where you can pay a bill using a Mastercard in Masterpass with no fee. Expires 9/30/18. Thanks to readers Jon and Bill. Here are the restrictions and details:

From now until September 30, 2018, we will waive the Plastiq fee when you use Mastercard in Masterpass for the payment. This promotion applies to any bills or invoices up to a maximum of $250 each.

To qualify for this promotion, you must:

Use a Mastercard in Masterpass for the payments (read here on how to add a Mastercard in Masterpass to your Plastiq account).

Submit or schedule payments between June 1, 2018 12:00 a.m. ET and September 30, 2018 11:59 p.m. ET.

The payments’ delivery date must be before or on September 30, 2018.

There is no minimum or maximum amount required for the transaction.

If the amount is over $250, you will incur a Plastiq fee on the remaining amount over $250.

If you have signed up with a referral code, you will need to hit the required minimum of $500 in successful payments and receive the fee-free dollar credit in order to be eligible for this promotion.

To clarify, there is a $250 limit per payment, but no limit on the number of payments. You could split up a larger bill into $250 increments if the payee accepts that. You could convert a mortgage, home equity loan, student loan, tuition, or property tax payment into a credit card payment that earns rewards or fulfill a sign-up bonus. For example, with the Citi Double Cash Card, the 2% cash back means every $5,000 in purchases could earn $100 cash back.

Original post:

Plastiq.com lets you pay bills and invoices with a credit or debit card, even if they don’t usually accept them. The standard service fee is 2.5% for credit cards and 1% for Visa and MasterCard debit cards. However, they run limited-time promotion with lower fees. They will charge your card and send out a paper check to the payee (direct bank transfers to a few), so you’d want to plan ahead for any snail mail delays. They recommend 10 business days to be safe. More ideas from their site:

- Rent or Mortgage

- Homeowners Association (HOA) dues

- Tuition

- Childcare costs

- Buying a car, RV, or ATV

- Income or business taxes

(Note: This was only an example given during a 1.5% fee promotion. The current fee may be higher or lower.) Why would I want to pay a 1.5% service fee?

Sign-up bonus spending requirements. Sign-up bonuses often having spending requirements. For example, you might get a $500 value bonus but need to spend $5,000. Well, that’s effectively 10% back so if you need a little help to get over that hurdle, it’s okay to pay a 1.5% fee. Here are some recent cards with big $500 value bonuses but also spending requirements:

- Chase Freedom Card

- BankAmericard Travel Rewards® Credit Card

- British Airways Credit Card

- Southwest Airlines Credit Card

- Chase Ink Plus Business Card

- Citi ThankYou Premier Card

- Citi Prestige Card

2% cash back credit cards, or similar. If you have a rewards credit card that offers 2% cash back (or equivalent value in points), then you can still make a slight profit by putting them on your credit card. A simple example is the Citi Double Cash Card. For example, if you have a tuition bill or tax bill of $5,000 and you earned 2% cash back while paying a 1.5% fee, your net 0.5% is $25.

Combine a rewards card + 0% APR on purchases. Many credit cards offer 0% APR on purchases for an introductory period of 12 months or longer. If the card also has a half-decent rewards program on purchases, the combination of purchase rewards and spreading out the payments over a year at no interest could be attractive.

Referral program. Plastiq has a somewhat confusing referral program. If a new user signs up via a referral link and pays $500 worth of bills, they will then get $500 “fee-free dollars”. So first you’d have to pay the fee on a bill, and then on your next bill, $500 of it will be “fee-free” (at 2.5% that’s a $12.50 savings). The referrer will get $1,000 in fee-free dollars. If you take advantage of the promo above, that should trigger the bonus. Here’s my referral link. Thanks if you use it.

Updated offers.

Updated offers.

Urbanr is an apartment rental website that allows renters to pay rent to landlords using a credit card. Urbanr accepts all Visa, MasterCard, and Discover credit and debit cards. The 1.5% transaction fee can be paid by renter, paid by the owner, or split evenly between them (owner pays 0.75% and the renter pays 0.75%). The owner/landlord must sign up on the service first to accept payments (direct deposited to their bank account).

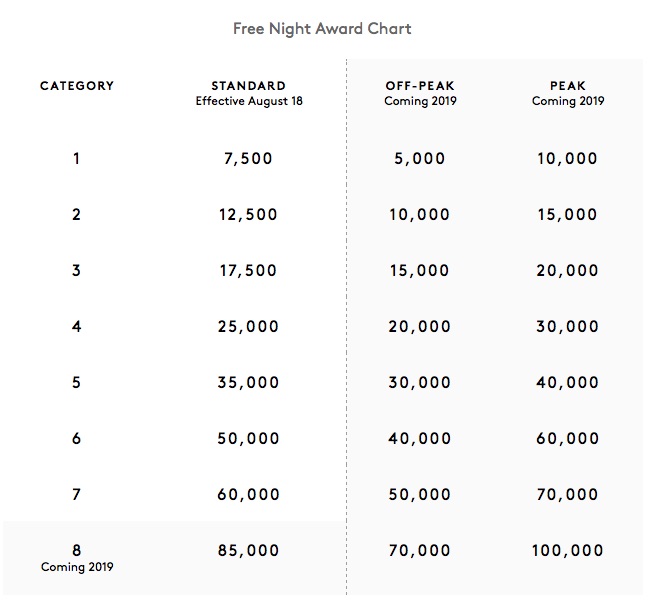

Urbanr is an apartment rental website that allows renters to pay rent to landlords using a credit card. Urbanr accepts all Visa, MasterCard, and Discover credit and debit cards. The 1.5% transaction fee can be paid by renter, paid by the owner, or split evenly between them (owner pays 0.75% and the renter pays 0.75%). The owner/landlord must sign up on the service first to accept payments (direct deposited to their bank account).  The Marriott Rewards Premier Plus Credit Card is the new co-branded card from Chase and the newly-merged Marriott/Starwood/Ritz-Carlton rewards program. The current bonus is 75,000 bonus Marriott Rewards points after spending $3,000 in 3 months. Here are the card highlights:

The Marriott Rewards Premier Plus Credit Card is the new co-branded card from Chase and the newly-merged Marriott/Starwood/Ritz-Carlton rewards program. The current bonus is 75,000 bonus Marriott Rewards points after spending $3,000 in 3 months. Here are the card highlights:

Barron’s has released their

Barron’s has released their  Interest rates are rising. Rate-chasing is becoming more worthwhile again. Here is my monthly roundup of the best safe rates available, roughly sorted from shortest to longest maturities. Check out my

Interest rates are rising. Rate-chasing is becoming more worthwhile again. Here is my monthly roundup of the best safe rates available, roughly sorted from shortest to longest maturities. Check out my  Amazon Prime has announced the following price increases to $119 per year:

Amazon Prime has announced the following price increases to $119 per year:

If you’ve already done a free trial of Audible.com and gotten some free audiobooks… Amazon might like to offer you another trial with

If you’ve already done a free trial of Audible.com and gotten some free audiobooks… Amazon might like to offer you another trial with

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)