If you can’t tell by now, I enjoy participating in various credit card, brokerage, and banking promotions throughout the year. I think of it as a profitable hobby, as I enjoy trying out different financial products in addition to the thousands of dollars in extra income each year. Below is the simple spreadsheet that I use to I track all of the various the requirements and deadline dates involved. I also set online calendar reminders using those dates.

If you can’t tell by now, I enjoy participating in various credit card, brokerage, and banking promotions throughout the year. I think of it as a profitable hobby, as I enjoy trying out different financial products in addition to the thousands of dollars in extra income each year. Below is the simple spreadsheet that I use to I track all of the various the requirements and deadline dates involved. I also set online calendar reminders using those dates.

I just moved it over to Google Sheets – the first link will allow you to make your own personal copy to edit as you wish. Please don’t ask for access to the original sheet, as that would mess it up for everyone else.

- MMB Simple Promotion Tracking Template (Make Your Own Copy To Edit)

- MMB Simple Promotion Tracking Template (View Only)

I intentionally keep it rather minimalist. This Reddit template by u/garettg is another example with many more bells and whistles.

See also: MMB Simple Portfolio Rebalancing Spreadsheet Template and How I store my physical credit cards.

Here’s my monthly roundup of the best interest rates on cash for October 2020, roughly sorted from shortest to longest maturities. I track these rates because I keep 12 months of expenses as a cash cushion and also invest in longer-term CDs (often at lesser-known credit unions) when they yield more than bonds. Check out my

Here’s my monthly roundup of the best interest rates on cash for October 2020, roughly sorted from shortest to longest maturities. I track these rates because I keep 12 months of expenses as a cash cushion and also invest in longer-term CDs (often at lesser-known credit unions) when they yield more than bonds. Check out my

Charles Munger is probably best known as the Vice Chairman of Berkshire Hathaway and longstanding investing partner of Warren Buffett. However, he has also been the CEO and/or Chairman of the Board of multiple other companies. This means there many additional sources of knowledge and wisdom beyond just

Charles Munger is probably best known as the Vice Chairman of Berkshire Hathaway and longstanding investing partner of Warren Buffett. However, he has also been the CEO and/or Chairman of the Board of multiple other companies. This means there many additional sources of knowledge and wisdom beyond just  Schwab has rolled out a new digital financial planning tool called

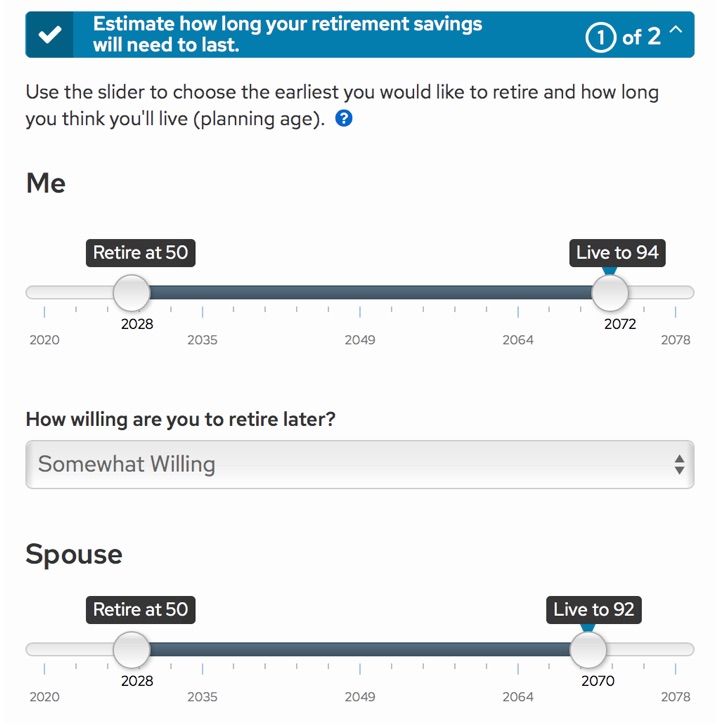

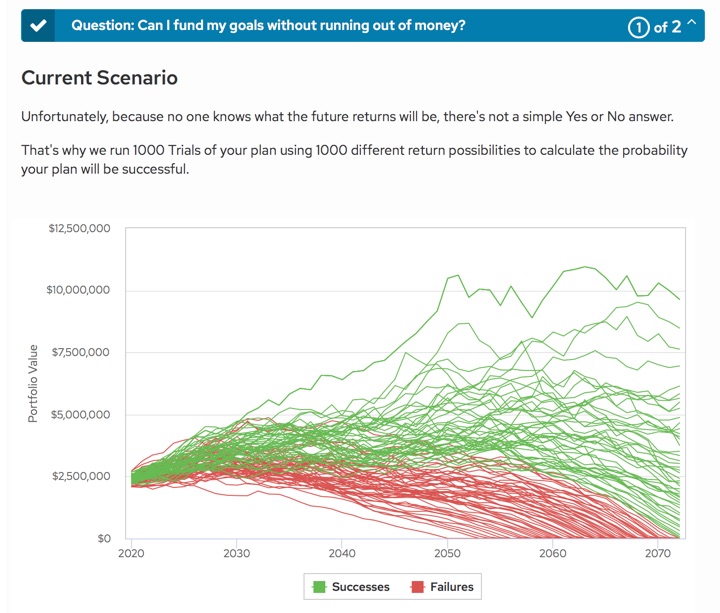

Schwab has rolled out a new digital financial planning tool called

Financial institutions increasingly want all of your money under one roof. Brokerage firms and robo-advisors are adding savings accounts and debit cards. Banks want to let you trade stocks. If you have built up some sizeable assets, you can make extra money when they decide to pay you to move over your assets. Try them out, see if you like them, and move again if you need to.

Financial institutions increasingly want all of your money under one roof. Brokerage firms and robo-advisors are adding savings accounts and debit cards. Banks want to let you trade stocks. If you have built up some sizeable assets, you can make extra money when they decide to pay you to move over your assets. Try them out, see if you like them, and move again if you need to. The CFA Institute Research Foundation publishes some short finance ebooks on Amazon Kindle that qualify as continuing education credits for Chartered Financial Analysts (CFAs), a type of investment professional certification.

The CFA Institute Research Foundation publishes some short finance ebooks on Amazon Kindle that qualify as continuing education credits for Chartered Financial Analysts (CFAs), a type of investment professional certification.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)