Another source of investment research and market commentary that I track is from Callan Associates. You may recall the name from their annual Callan Periodic Table of Returns. In addition to that, Callan offers free access to their entire Research Library with your e-mail address. Their focus is on institutional investors, but there are often things of interest for motivated individual investors. Some of my highlights from their 1st Quarter 2016 papers:

A discussion of investing in “real” assets such as real estate, TIPS, and commodities. As they point out, the best time to consider an inflation hedge is when the risk is considered low. Here a chart of 15-year historical returns vs. volatility for various asset classes.

I would note that it can be very difficult (if not impossible) for an individual investor to get low-cost, diversified, direct access to certain asset classes like timberland and farmland. There are some ETFs being marketed, but they do not provide pure exposure. If you have many millions if not billions, not a problem.

10-year capital market projections. Each year, they share 10-year projected returns for major asset classes. They also go out on a limb and make predictions about expected standard deviation and correlations, which I think is rather bold (and thus I shall ignore it). Below is a partial snapshot (click to enlarge). Download their full report for the test.

Returns are nominal, and their inflation projection is 2.3%. If you are looking for a more optimistic outlook, Callan’s projections are overall higher than many others I have seen. If the predictions of +7.4% annualized returns for US Stocks, +7.6% for International Stocks, and +3% for US Bonds all hold, I will be a happy camper.

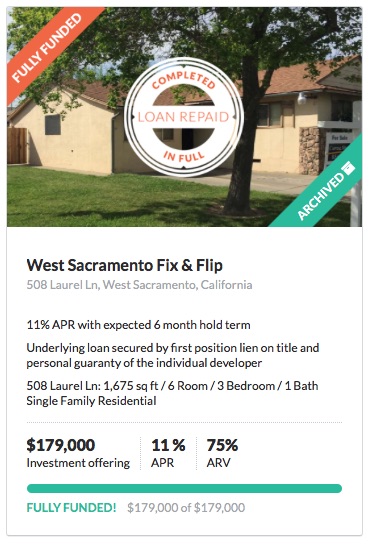

My first investment into real estate crowdfunding has completed. In April 2015, I invested $5,000 into a fix-and-flip loan at the site

My first investment into real estate crowdfunding has completed. In April 2015, I invested $5,000 into a fix-and-flip loan at the site

I like the idea of living off dividend and interest income. Who doesn’t? The problem is that you can’t just buy stocks with the absolute highest dividend yields and junk bonds with the highest interest rates without giving up something in return. There are many bad investments lurking out there for desperate retirees looking only at income. My goal is to generate reliable portfolio income by not reaching too far for yield.

I like the idea of living off dividend and interest income. Who doesn’t? The problem is that you can’t just buy stocks with the absolute highest dividend yields and junk bonds with the highest interest rates without giving up something in return. There are many bad investments lurking out there for desperate retirees looking only at income. My goal is to generate reliable portfolio income by not reaching too far for yield. It has been a while, so here is a 2016 First Quarter update on my investment portfolio holdings. This includes tax-deferred accounts like 401ks, IRAs, and taxable brokerage holdings, but excludes things like our primary home and cash reserves (emergency fund). The purpose of this portfolio is to create enough income to cover household expenses.

It has been a while, so here is a 2016 First Quarter update on my investment portfolio holdings. This includes tax-deferred accounts like 401ks, IRAs, and taxable brokerage holdings, but excludes things like our primary home and cash reserves (emergency fund). The purpose of this portfolio is to create enough income to cover household expenses.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)