Another online ETF portfolio advisor joins the mix. Discount brokerage TradeKing, possibly best known for their $4.95 stock trades, announced a new subsidiary called TradeKing Advisors which will directly manage ETF portfolios for retail customers. Details:

Another online ETF portfolio advisor joins the mix. Discount brokerage TradeKing, possibly best known for their $4.95 stock trades, announced a new subsidiary called TradeKing Advisors which will directly manage ETF portfolios for retail customers. Details:

- Portfolio asset allocation designed and monitored by Ibbotson Associates. There will be Core and Momentum portfolios.

- The portfolio will be determined by an 8 question risk questionnaire.

- TradeKing Advisors will manage and rebalance portfolio as needed to stay on target. Assets will be held at TradeKing brokerage.

- Management fee of 0.75% of account balance annually for Core portfolios, minimum initial investment of $10,000. For Momentum portfolios, 1% management fee and $25k minimum account size. For account balances over $250,000, the fees for each portfolio are reduced to 0.50% annually.

Per their website, their “strategies include a diversified allocation of up to 20 asset classes – including fixed income, equities, real estate and foreign investments – implemented cost-effectively with ETFs.” I could not find any specific information about the asset allocation of these ETF portfolios or the ticker symbols used.

But that’s okay, as I pretty much stopped listening when the fees were listed at 0.75% for a basic index ETF portfolio. It may be less than what E*Trade charges but in my opinion that’s still too much to pay for any ETF portfolio, and much more than many other services like Betterment and Wealthfront that do pretty much the same thing also with a slick user interface. Supposedly TradeKing will differentiate themselves with their “exceptional customer service”. As a TradeKing brokerage customer, I found their customer service fine and Live Chat is nice but not worth another 0.40% to 0.50% annually as you don’t even get assigned a Certified Financial Planner or CFA. So far it just sounds like an expensive robo-advisor. In that case, I will pass.

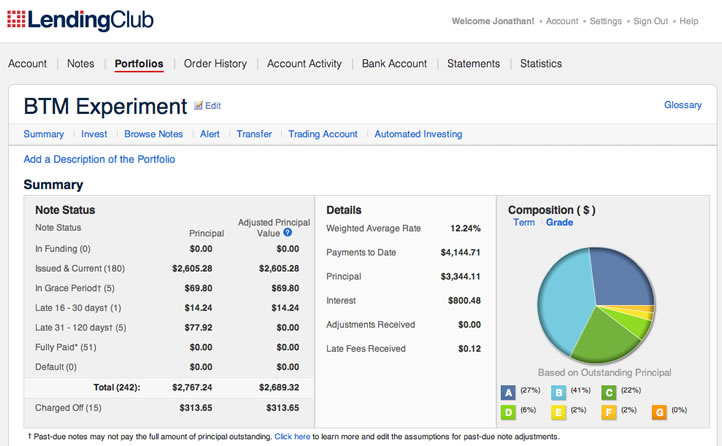

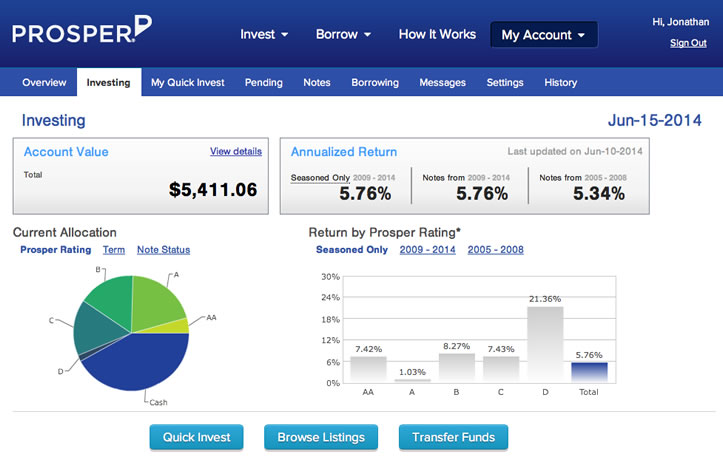

In November 2012, I invested $10,000 into person-to-person loans split evenly between

In November 2012, I invested $10,000 into person-to-person loans split evenly between

Just as important as finding a good investment is knowing what investments to avoid at all costs. If you simply manage to avoid putting any money into financial sinkholes, you’ll come out ahead. I’ve already mentioned the common mistake of

Just as important as finding a good investment is knowing what investments to avoid at all costs. If you simply manage to avoid putting any money into financial sinkholes, you’ll come out ahead. I’ve already mentioned the common mistake of  I just finished reading

I just finished reading  Many people hire a financial advisor because they aren’t comfortable investing on their own, and they appreciate having an experienced person to talk to whenever they have any questions. However, this has traditionally meant paying at least 1% of your portfolio assets every year to that person. Especially given the current low interest rate environment, 1% is a huge number and could eat up a large percentage of your future returns.

Many people hire a financial advisor because they aren’t comfortable investing on their own, and they appreciate having an experienced person to talk to whenever they have any questions. However, this has traditionally meant paying at least 1% of your portfolio assets every year to that person. Especially given the current low interest rate environment, 1% is a huge number and could eat up a large percentage of your future returns. Being a peer-to-peer lender been a bumpy ride.

Being a peer-to-peer lender been a bumpy ride.  The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)