Many online banking, stock trading, crypto, and fintech apps use the Plaid service to provide easy funding via your existing bank accounts. The price of this convenience is that you are providing some very sensitive data to a small, private company. They have your bank login information and can see all your transaction data. (Visa was in an agreement to acquire Plaid for over $5 billion, but it was cancelled to due antitrust concerns.) A recent Plaid class action lawsuit alleges the following improper actions:

Many online banking, stock trading, crypto, and fintech apps use the Plaid service to provide easy funding via your existing bank accounts. The price of this convenience is that you are providing some very sensitive data to a small, private company. They have your bank login information and can see all your transaction data. (Visa was in an agreement to acquire Plaid for over $5 billion, but it was cancelled to due antitrust concerns.) A recent Plaid class action lawsuit alleges the following improper actions:

The allegations include that Plaid: (1) obtained more financial data than was needed by a user’s app, and (2) obtained log-in credentials (username and password) through its user interface, known as “Plaid Link,” which had the look and feel of the user’s own bank account login screen, when users were actually providing their login credentials directly to Plaid. Plaid denies these allegations and any wrongdoing and maintains that it adequately disclosed and maintained transparency about its practices to consumers.

(You may have gotten an e-mail about this as early as mid-January. Thanks to those who sent it in as well. I still managed to forget about it until writing a post about firewall bank accounts to avoid such data privacy concerns.)

If you connected your financial account(s) to a mobile or web-based app that has used Plaid between January 1, 2013 and November 19, 2021 in the United States, you may be eligible for a payment from this class action Settlement. This might include Venmo, Robinhood, Chime, SoFi, Coinbase, OnJuno, Lili, M1 Finance, or Blockfi just off the top of my head. I don’t have any special insights about the merits of this lawsuit, but the proposed settlement amount is for $58 million with the payout per claim being unknown. The settlement also requires Plaid to:

- Delete certain data from Plaid systems;

- Inform Class Members of their ability to use Plaid Portal to manage the connections made between their financial accounts and chosen applications using Plaid and delete data stored in Plaid’s systems;

- Continue to include certain disclosures and features in Plaid’s standard Link flow;

- Enhance disclosures about Plaid’s data collection practices, how Plaid uses data, and privacy controls Plaid has made available to uses in Plaid’s End User Privacy Policy;

- Minimize the data that Plaid stores; and

- Continue to host a dedicated webpage with detailed information about Plaid’s security practices.

The deadline to submit a claim is April 28, 2022.

Here’s my monthly roundup of the best interest rates on cash as of March 2022, roughly sorted from shortest to longest maturities. I look for lesser-known opportunities available to individuals while still keeping your principal FDIC-insured or equivalent. I use this information for both my cash reserves and as possible bond substitutes. Check out my

Here’s my monthly roundup of the best interest rates on cash as of March 2022, roughly sorted from shortest to longest maturities. I look for lesser-known opportunities available to individuals while still keeping your principal FDIC-insured or equivalent. I use this information for both my cash reserves and as possible bond substitutes. Check out my

WeBull 12 Free Fractional Stocks Offer

WeBull 12 Free Fractional Stocks Offer SoFi Invest Free $25 in Stock Offer

SoFi Invest Free $25 in Stock Offer TradeUP Free Stocks Offer

TradeUP Free Stocks Offer Public Free Stock Offer

Public Free Stock Offer Robinhood Free Stock Offer

Robinhood Free Stock Offer Did you know that there exists a tuition-free, accredited, online university where you can obtain an Bachelor’s degree in Computers Science, MBA, or Masters in Education for a tiny fraction of the cost of traditional universities? The

Did you know that there exists a tuition-free, accredited, online university where you can obtain an Bachelor’s degree in Computers Science, MBA, or Masters in Education for a tiny fraction of the cost of traditional universities? The

Amazon Prime has announced the following price increases (note that some links will show up if you are viewing this via e-mail newsletter, please read online):

Amazon Prime has announced the following price increases (note that some links will show up if you are viewing this via e-mail newsletter, please read online):

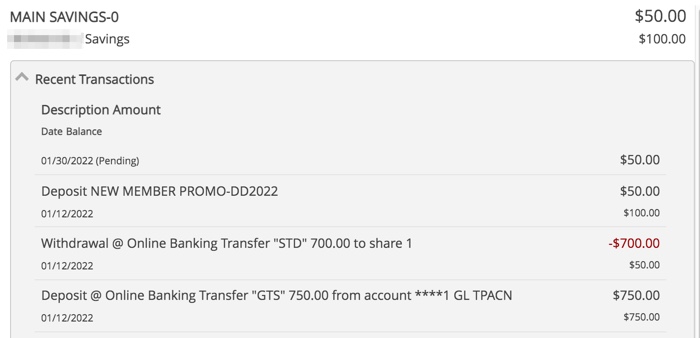

Lafayette Federal Credit Union (LFCU) has a respectable history of offering competitively-priced banking products. I recently joined and here is a quick review of their current promotions and the application process. Highlights:

Lafayette Federal Credit Union (LFCU) has a respectable history of offering competitively-priced banking products. I recently joined and here is a quick review of their current promotions and the application process. Highlights:

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)