Last Friday, the yield on the 10-year US Treasury note was a tiny bit less than that of the 3-month US Treasury bill. This is known as a yield inversion, and depending on which article you read, this specific type of yield inversion (10-year minus 3-month) has happened before each of the past 6, 7, or 9 recessions. More overview in this Bloomberg article:

Here is a FRED chart showing the difference between the 10-year and 3-month yields since 1978. The gray areas are recessions. (Click to enlarge.)

Yield inversion. Recession. Yield inversion. Recession. Every time.

This does not necessarily mean you should sell all your stocks now. You can see for yourself that there is a bit of lag time between the initial inversion and the official start of a recession. The length of time can vary, and it could be years. That means if you jump out of stocks now, things might still go up for a while. In addition, there’s no way to know the length or severity of the recession. How will you know when to jump back in stocks again? Lots of people sat out 2008 through 2018.

In my opinion, this is like your local fire department knocking on your door and reminding you to make an emergency plan for whatever disasters you are exposed to – fire, earthquakes, tornadoes, hurricanes. A hurricane may not hit soon, or even this year, or the next. You make the plan now, so you will be prepared and know exactly what to do when it does eventually hit.

You should know that you are going to do in a recession before the recession actually hits.

- What will you do if you lose your job and can find another one immediately? What if your business revenue drops significantly?

- Do you know what areas of spending you would cut if you really needed to? What can you liquidate easily for cash?

- What will you do if your stocks lose up to 50% in value and stay that way for years? Will you hold? Sell or rebalance according to a preset rule?

- What will you do if your home value drops by 20% or more?

- Where can you borrow money if needed? Are you sure that line of credit will still be there?

I’ve thought about most of this, but I should create a written plan that my partner can follow even if I’m not around.

One of the biggest problems in retirement planning is turning a pile of money into a reliable stream of income. I have read hundreds of articles about this topic, and I have not yet found a perfect solution to this problem. Everything has pros and cons: stocks, high-dividend stocks, bonds, annuities, real estate, and so on.

One of the biggest problems in retirement planning is turning a pile of money into a reliable stream of income. I have read hundreds of articles about this topic, and I have not yet found a perfect solution to this problem. Everything has pros and cons: stocks, high-dividend stocks, bonds, annuities, real estate, and so on.

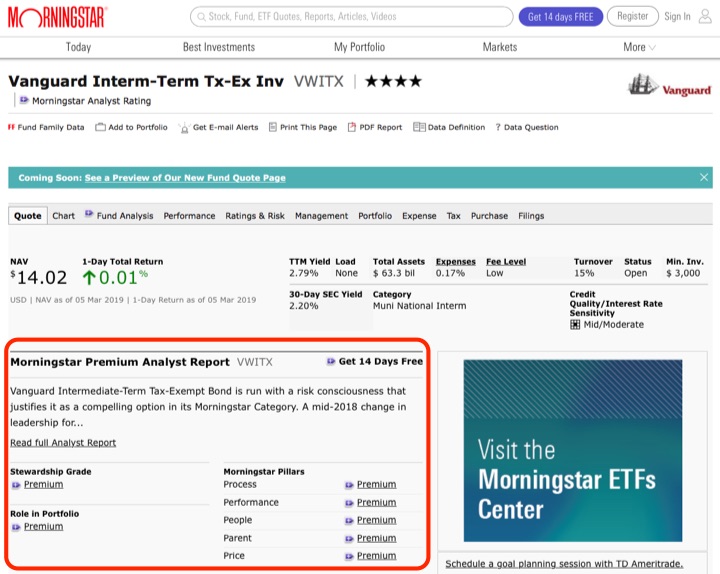

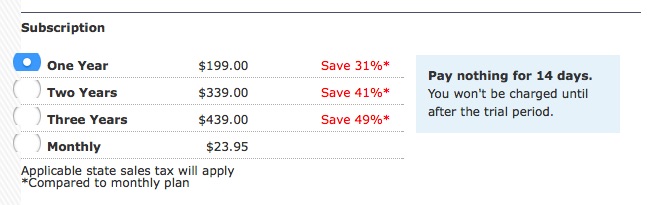

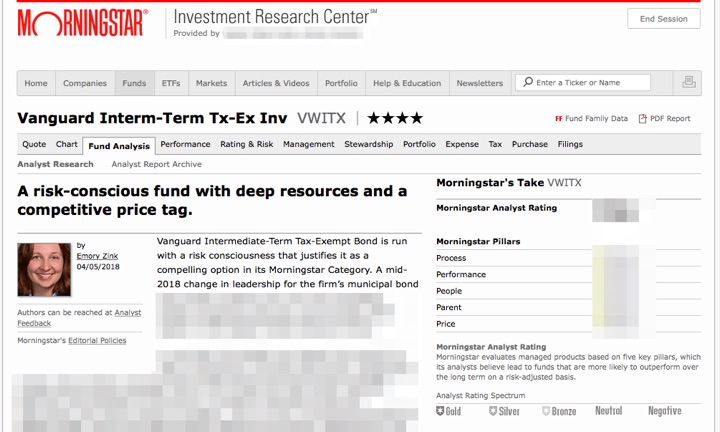

Updated 2019. Let’s say you are a DIY investor and doing some research on some mutual funds. You decide to learn more about the Vanguard Intermediate-Term Tax-Exempt Fund. You pull up the Morningstar quote pages (ticker

Updated 2019. Let’s say you are a DIY investor and doing some research on some mutual funds. You decide to learn more about the Vanguard Intermediate-Term Tax-Exempt Fund. You pull up the Morningstar quote pages (ticker

Here’s my monthly roundup of the best interest rates on cash for March 2019, roughly sorted from shortest to longest maturities. Check out my

Here’s my monthly roundup of the best interest rates on cash for March 2019, roughly sorted from shortest to longest maturities. Check out my  T. Rowe Price has an article

T. Rowe Price has an article

Berkshire Hathaway (BRK) has released its

Berkshire Hathaway (BRK) has released its  The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)