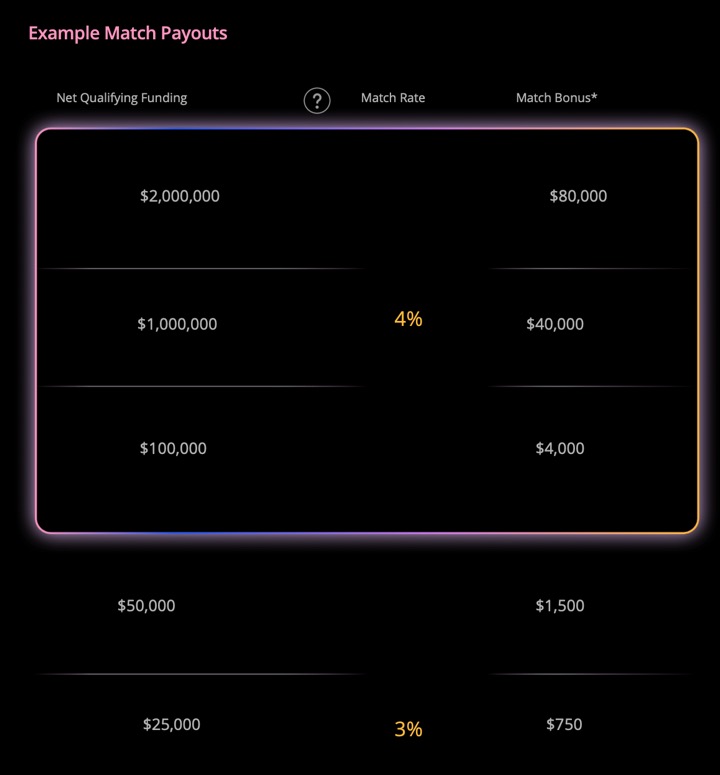

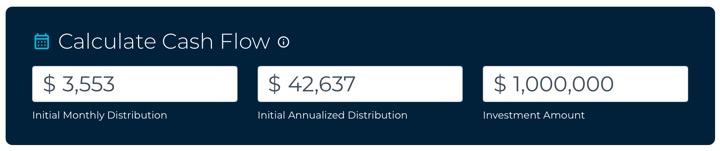

Updated with new offer. The Webull brokerage app is offering an updated ACAT Transfer bonus of up to 4% of assets transferred plus up to $100 in outgoing fee reimbursements on your first transfer of at least $2,000. This specific offer ends March 31, 2026. This is for individual taxable brokerage accounts. Joint, Crypto, and IRA accounts are excluded.

You must transfer at least $100,000 in assets to get a 4% match, with a minimum hold of 5 years to get the full payout (they break it up into installments with the last one being paid March 2031). Max funding is $2,000,000. You must transfer at least $2,000 in assets to get a 3% match, also with a minimum hold of 5 years. 4% is a very high bonus, but it is a long hold period. Be sure to read all the terms and conditions.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)