Updated and revised 2013. You often hear that stock investing is a sure thing over the “long run”. But as this chart from the NY Times and Crestmont Research shows, there is still a lot of variability involved. The matrix below visually displays the annualized returns for the S&P 500 for every starting and ending year from 1920 to 2010, adjusted for inflation, taxes, and transaction costs.

(click to enlarge)

Your actual returns depend a lot upon when you start, and also when you finally withdraw:

After accounting for dividends, inflation, taxes and fees, $10,000 invested at the end of 1961 would have shrunk to $6,600 by 1981. From the end of 1979 to 1999, $10,000 would have grown to $48,000.

“Market returns are more volatile than most people realize,” Mr. Easterling said, “even over periods as long as 20 years.”

Some further observations:

[Read more…]

Yesterday, I posted a

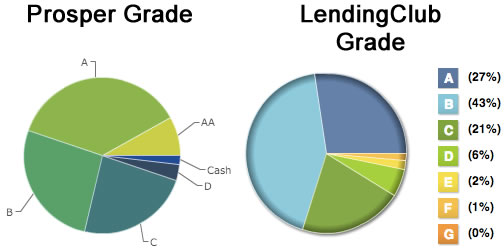

Yesterday, I posted a  I invested $10,000 into person-to-person loans in November 2012, split evenly between

I invested $10,000 into person-to-person loans in November 2012, split evenly between

I’ve written about how recent fee disclosure requirements for 401(k) retirement plans have brought a spotlight on

I’ve written about how recent fee disclosure requirements for 401(k) retirement plans have brought a spotlight on

I’ve read a few books about dividend investing and remain interested in the idea, although I’m not confident enough (yet?) to allocate my portfolio that way. Portfolio manager and writer Mebane Faber has a short book called

I’ve read a few books about dividend investing and remain interested in the idea, although I’m not confident enough (yet?) to allocate my portfolio that way. Portfolio manager and writer Mebane Faber has a short book called  Along with other factors, new fee disclosure requirements for 401(k) plans have brought a lot of attention recently on “bad” 401(k) plans. These are plans with little or no employer match, higher-than-average fees, and/or limited investment choices.

Along with other factors, new fee disclosure requirements for 401(k) plans have brought a lot of attention recently on “bad” 401(k) plans. These are plans with little or no employer match, higher-than-average fees, and/or limited investment choices.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)