T. Rowe Price has an article Evaluating Roth and Pretax Retirement Savings Options by Roger Young that covers the basics on the choice between a “Traditional” pretax or Roth IRA or 401k account:

T. Rowe Price has an article Evaluating Roth and Pretax Retirement Savings Options by Roger Young that covers the basics on the choice between a “Traditional” pretax or Roth IRA or 401k account:

The primary factor to consider is whether your marginal tax rate will be higher or lower during retirement. If your tax rate will be higher later, paying taxes now with the Roth makes sense. If your tax rate will be lower, you want to defer taxes until then by using the pretax approach.

With the Traditional pretax, you get to avoid paying income taxes on the contribution now, but you must pay taxes up on withdrawal. With the Roth, you pay income taxes now, but you don’t own any taxes upon withdrawal. However, I am linking to it because it also includes a table with some sample worker profiles. This may help clarify things for people who are still confused about which to pick.

There are other considerations due to our overly-complex tax code, but I think this is still a helpful tool.

Individual Retirement Arrangements (IRAs) are way to save money towards retirement that also saves on taxes. For 2019, the annual contribution limit for either Traditional or Roth IRAs increased to $6,000 (it is roughly indexed to inflation). The additional catch-up contribution allowed for those age 50+ stays at $1,000 (for a total of $7,000). You can’t contribute more than your taxable compensation for the year, although a spouse can contribute with no income if the other person has enough income.

Individual Retirement Arrangements (IRAs) are way to save money towards retirement that also saves on taxes. For 2019, the annual contribution limit for either Traditional or Roth IRAs increased to $6,000 (it is roughly indexed to inflation). The additional catch-up contribution allowed for those age 50+ stays at $1,000 (for a total of $7,000). You can’t contribute more than your taxable compensation for the year, although a spouse can contribute with no income if the other person has enough income.

Employer-based retirement plans like the 401(k), 403(b), and Thrift Savings Plan are not perfect, but they are often the best available option to save money in a tax-advantaged manner. For 2019, the employee elective deferral (contribution) limit for these plans increased to $19,000 (it is indexed to inflation). The additional catch-up contribution allowed for those age 50+ stays at $6,000 (for a total of $25,000).

Employer-based retirement plans like the 401(k), 403(b), and Thrift Savings Plan are not perfect, but they are often the best available option to save money in a tax-advantaged manner. For 2019, the employee elective deferral (contribution) limit for these plans increased to $19,000 (it is indexed to inflation). The additional catch-up contribution allowed for those age 50+ stays at $6,000 (for a total of $25,000).

Instead of just looking at one year of returns, I prefer taking a longer view. Most successful savers invest money each year over a long period of time, these days often into a target-date fund (TDF). Don’t get caught up in the daily news reporting the recent performance of the Dow or S&P 500.

Instead of just looking at one year of returns, I prefer taking a longer view. Most successful savers invest money each year over a long period of time, these days often into a target-date fund (TDF). Don’t get caught up in the daily news reporting the recent performance of the Dow or S&P 500.

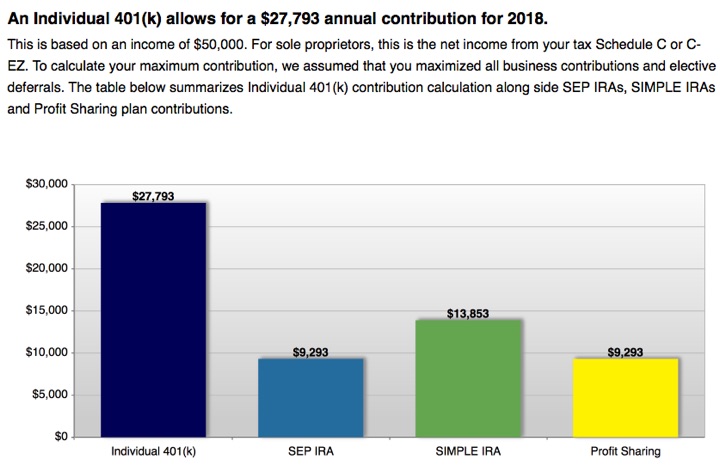

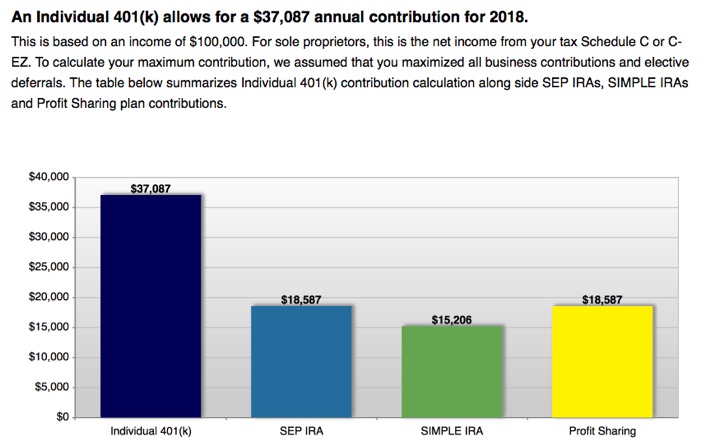

Each December, I run the numbers to see how much more I can contribute to my Self-Employed 401k plan, aka Solo 401k or Individual 401k.

Each December, I run the numbers to see how much more I can contribute to my Self-Employed 401k plan, aka Solo 401k or Individual 401k.

This is not a happy post, but it’s also the reality for a lot of people so I think it is a valid discussion. The Early Retirement forums had a thread recently titled

This is not a happy post, but it’s also the reality for a lot of people so I think it is a valid discussion. The Early Retirement forums had a thread recently titled  Here’s a refreshingly blunt quote from Scott Galloway’s article

Here’s a refreshingly blunt quote from Scott Galloway’s article  The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)